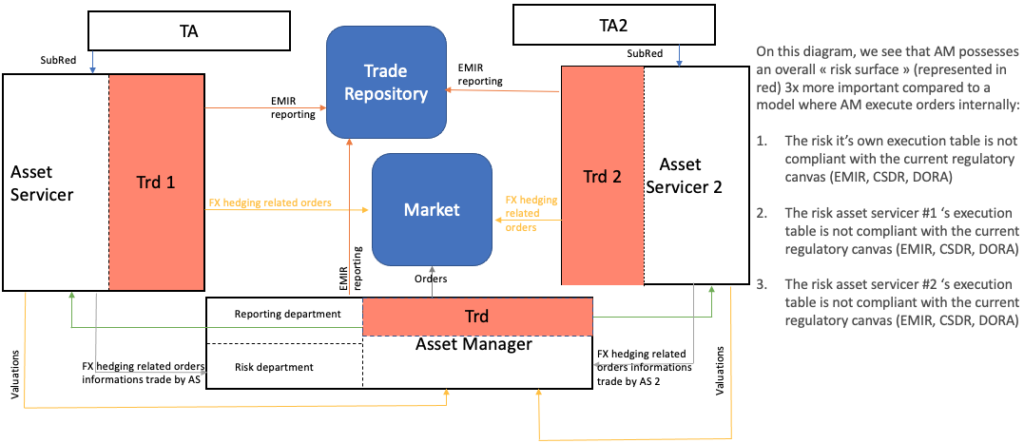

MIFID clearly states that Asset Managers will ultimately bear final responsiblility for any wrong doing by the execution tables

For an Asset Manager

4 main issues compared to an operating model where FX hedging related orders are in-house:

- Booking risk

- Operational risk

- Collateral optimization

- Regulatory risk

Booking risk:

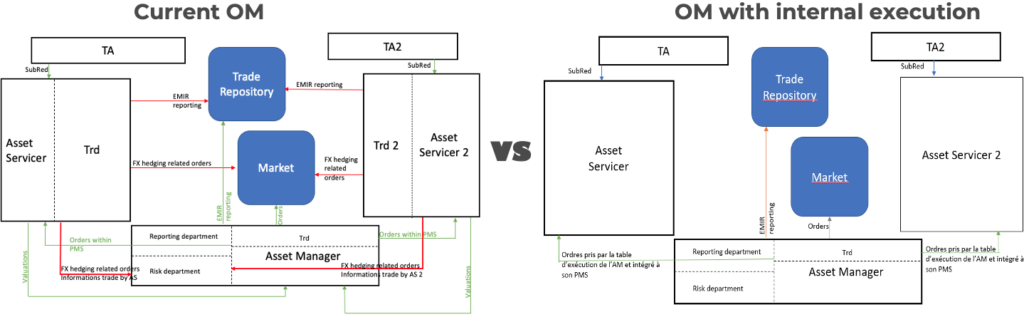

Currently AM must integrate all FX hedging related orders (red one particularly as it is traded by an asset servicer outside its IT) into their own PMS to reflect the correct fund asset composition. To do so, asset manager’s IT must create and maintain channels between the asset servicer and the asset manager to retrieve the necessary information (fully and on time).

Failure to collect those FX hedging related orders taken outside their PMS will lead to:

- wrong risk metrics (as the short forward is not feeding into the asset manager’s PMS/risk department)

- regulatory breaches

Operational risk:

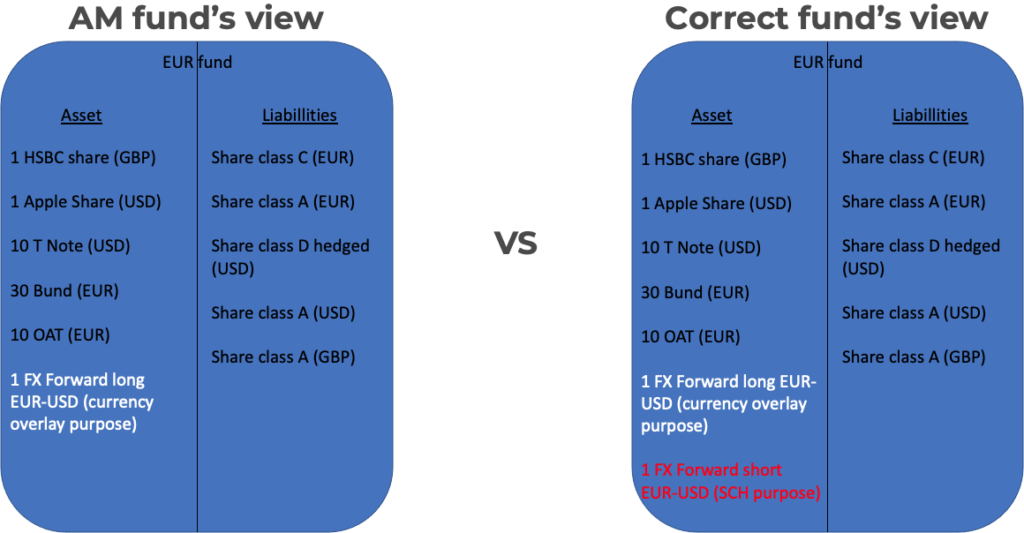

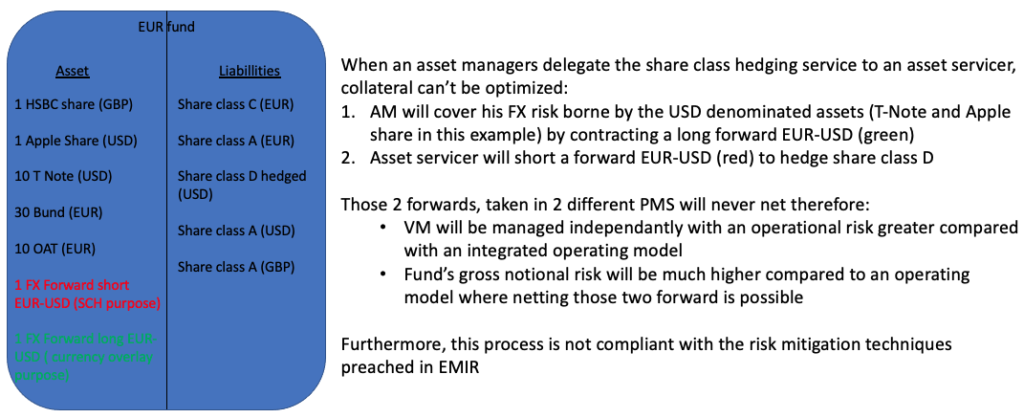

Collateral optimization:

This problem stems from the fact that, historically, AM manages funds assets and delegate liability management to an asset servicer (fund admin…).

Regulatory risk:

To see why the AMF inflicted a 500.000€ fine to an asset servicer for EMIR non compliance :

Overall, this setup leaves Asset Managers with :

- Strong dependencies to asset servicers

- Bigger exposure to regulatory breaches

- No control but full responsibility over it

Moreover, with CSDR implementation, AM will probably pay a higher price due to an increase in complexity of execution. It will certainly have to revise the legal documentation to establish and maintain a list of counterparties with the least rate of failure as well as procedures on ways they will allocate fines/ bonuses delivered by CSD.

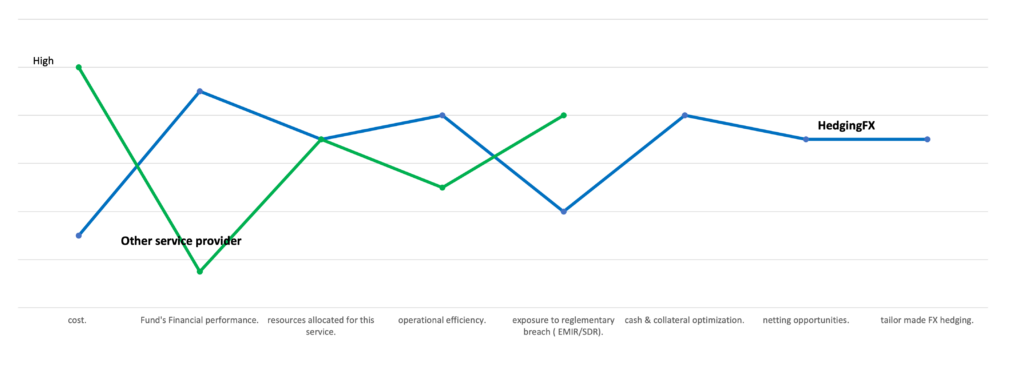

By internalizing execution, AM will:

- Increase fund’s financial performance (up to several bp/year per hedged share class)

- Increase their optimization of their collateral (both in amount and opportunities)

- Increase operational efficiency (by enhancing their trading desk and also compliance teams, legal and risk)

- Divide their exposure to regulatory breach

- Tailor made their client’s hedging

HedgingFX was also able to secure a partnership with a leading insurance company which agreed to cover any potential miscalculation risk from up to 4 millions Euros.

For an investment bank

The best of two worlds

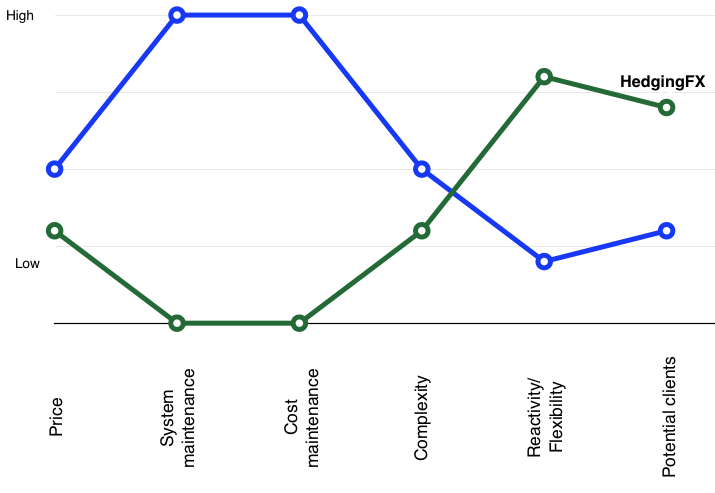

As an investment banker, maintaining this tool in production is extremely costly and requires numerous staff from different teams.

Scalability is often an issue and assessing any upgrade turns out to be costly and time consuming leading to client’s dissatisfaction.

HedgingFX, leaning on its small structure with a high degree of expertise, tackles those issues with a flexible and scalable environment. Assessing any upgrade’s request from your clients is always done in a timely manner.